Indonesia Residential Market Report 2023 & Outlook 2024

EXECUTIVE SUMMARY

VAT Exemption Program Stimulus

The VAT exemption program stimulated a double increase in the addition of inventory (supply) for new housing projects and drove a 27% growth in the demand for new homes by the end of 2023.

Home Financing Adaptations

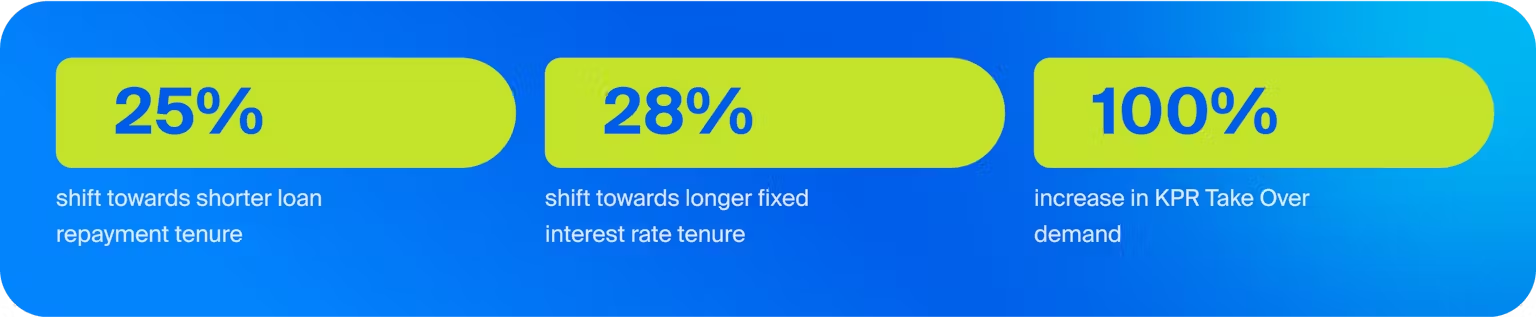

Interest rate hikes have driven demand for shorter loan repayment periods and longer fixed interest rates, as well as an increase in KPR Take Over demand.

Urbanization and Rental Demand

The post-pandemic era, which has spurred urbanization, has made DKI Jakarta and Bandung, along with their surrounding cities, become a preferred locations for renting houses.

Market Outlook 2024

Preference in residential is on the rise in areas with undergoing infrastructure development and tourism sector recovery.

MARKET REPORT

∙

Written by Pinhome Research Team

∙

14 March 2024

Housing Inventory Evolution: Response to Incentives and Infrastructure Development

The announcement of the VAT exemption program in November 2023 became a significant catalyst in the dynamics of the property market, especially in the new home segment. This decision triggered a significant surge with a double monthly increase (MoM) in the addition of new inventory for housing projects. It reflects the optimism and positive response of market players.

+12%

+12% Housing projects priced below IDR 300 million

shows a 12% monthly growth in the addition of new inventory in November 2023, indicating increased ownership access for first-time homebuyers and investors.

+115%

+115% The construction of the

Serpong-Bogor via Parung toll road

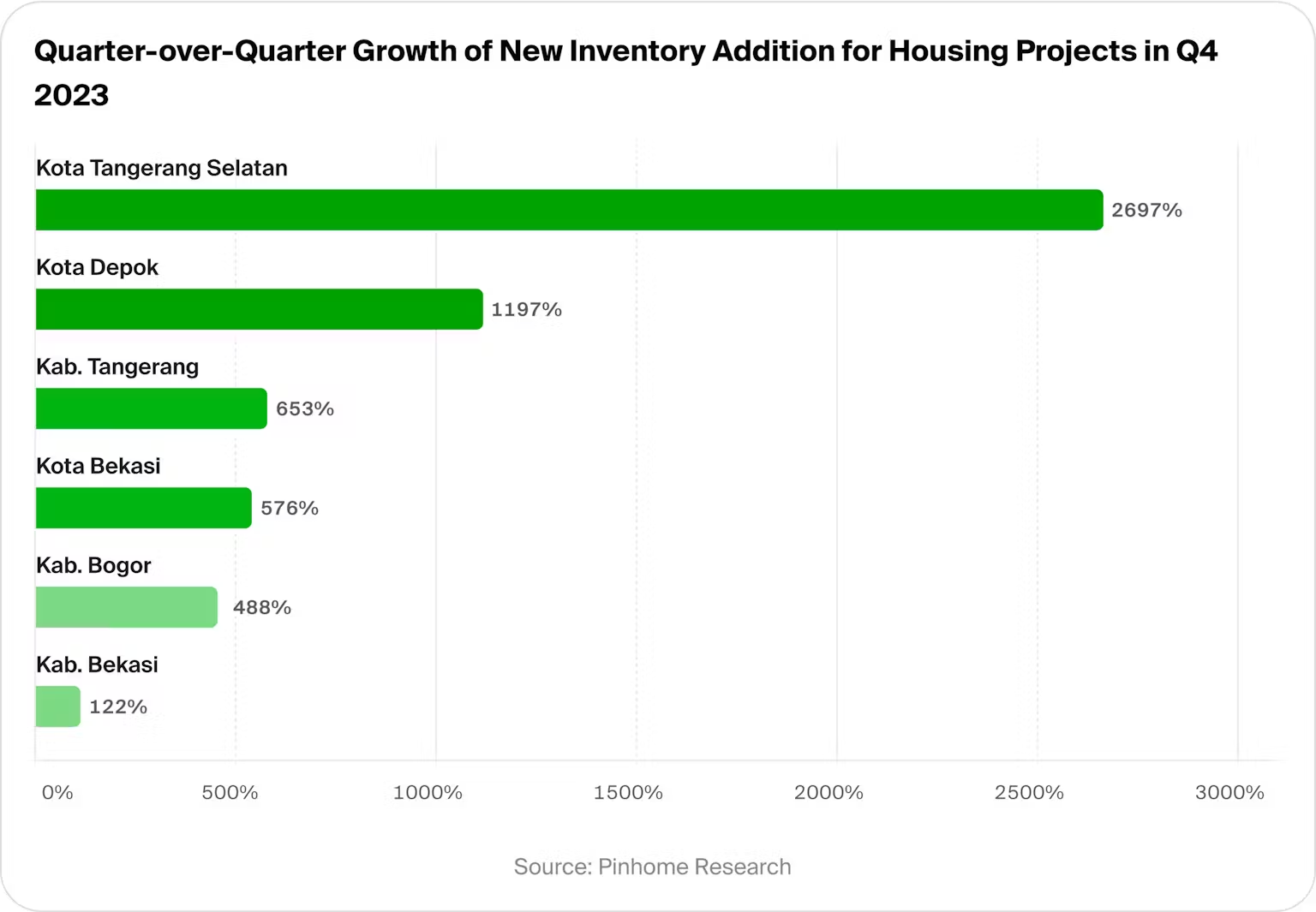

has had a strong impact on the addition of new inventory for housing projects in Bogor Regency, with more than a doubling of the inventory of new home projects in September 2023.

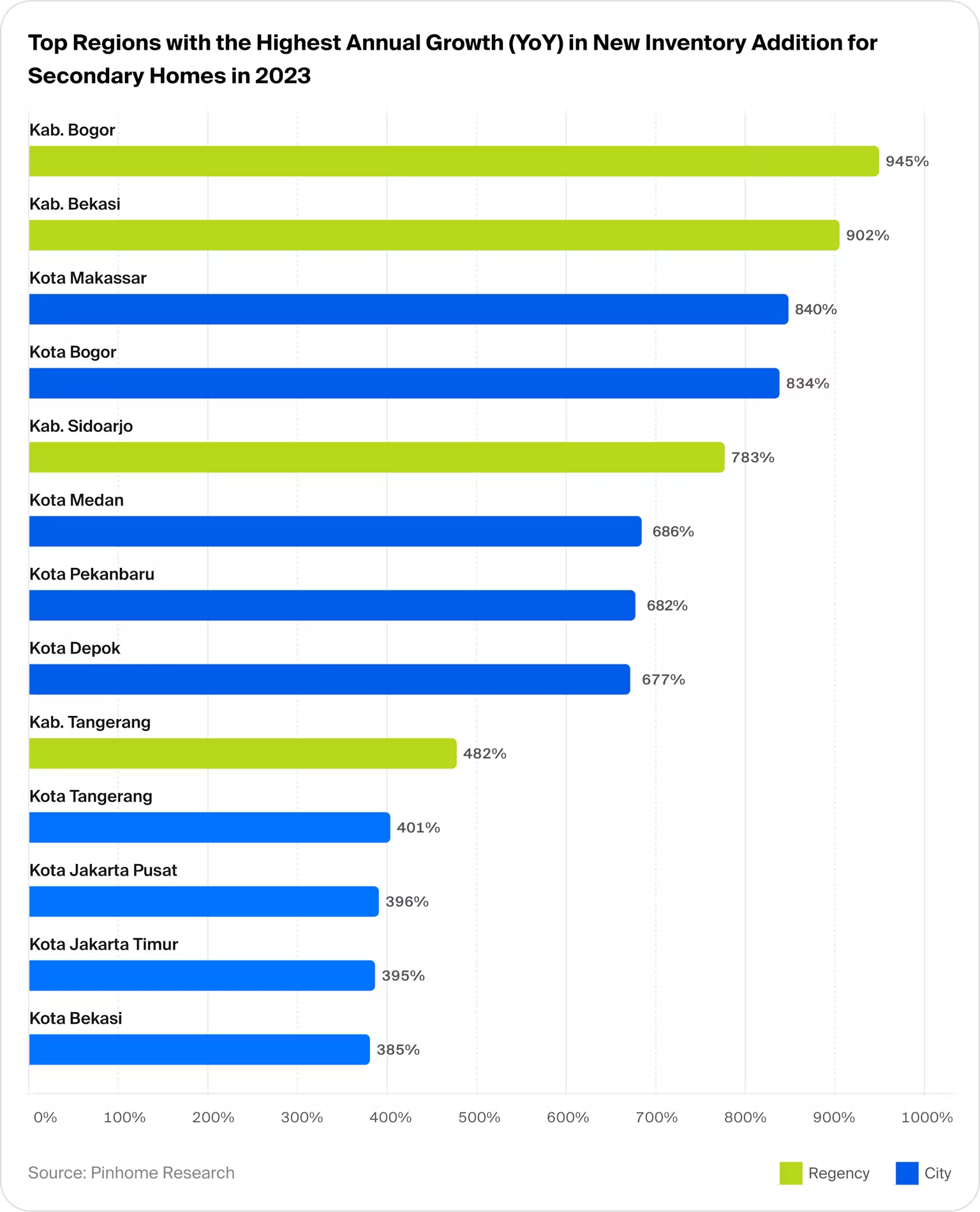

The secondary home inventory also experienced interesting dynamics throughout the year, with consistent growth in the addition of new inventory despite a temporary decline during the Eid al-Fitr holiday and the October-November 2023 period in some provinces. However, West Java managed to maintain the growth of new inventory for secondary homes, affirming the market's resilience in the region. Furthermore, the growth of new inventory for secondary homes on a regional level showed a significant increase in regency areas, with Bogor and Bekasi experiencing an increase of up to ninefold from 2022 to 2023, followed by Sidoarjo.

new inventory addition for housing projects and secondary home

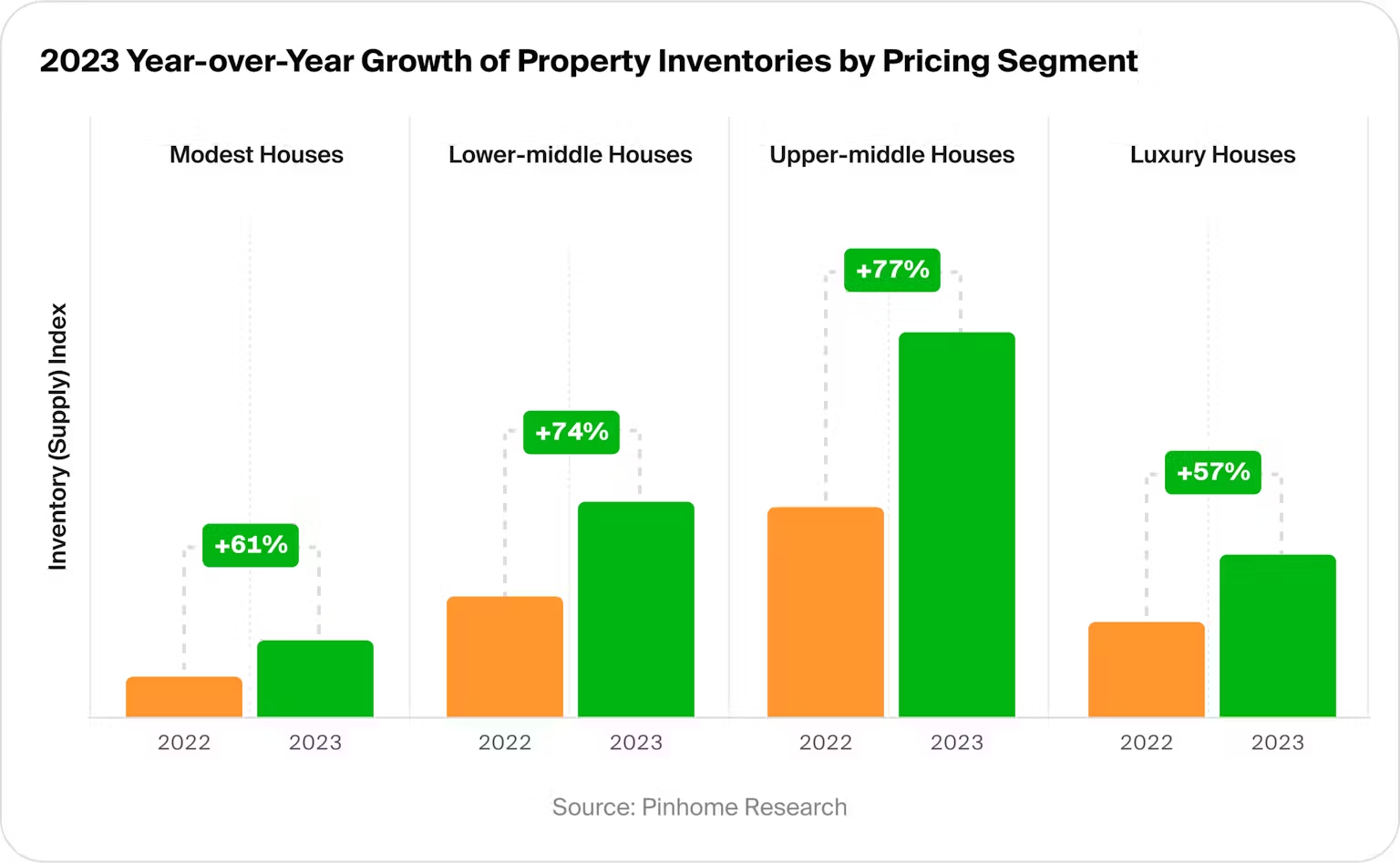

in 2023 grew by 56% compared to 2022.

Inventory for modest houses

showed an annual growth of up to 61%, with significant spikes occurring in Bogor and Tangerang Raya increasing more than 160% annually.

Inventory for lower-middle houses

showed an annual growth of 74%, with Depok managing to grow more than tenfold annually.

Inventory for upper-middle houses

showed an annual growth of 77%, with Depok and Surabaya leading as the cities with the highest annual growth in this segment at 180%.

The growth of luxury houses

in Surabaya showed a stable growth, with an annual growth rate of 177%. Not only that, Bogor, Depok and Tangerang Raya, in addition to offering alternatives for affordable houses, also expand their luxury house options with at least 40% annual growth.

House Buying Demand Trend: Incentive Stimulus and Infrastructure Development

The Indonesia government provides incentive in the form of a full VAT exemption (100%) for the purchase of the first home with a selling price of up to IDR 2 billion and a VAT reduction for homes with a selling price above IDR 2 billion up to IDR 5 billion. This incentive provided a stimulus for new housing demand at the end of 2023, recording a monthly growth of 27% from November to December 2023. This marks a strong market response to this fiscal incentive.

-

The Jabodetabek region recorded the most significant surge in demand following the announcement of the VAT-free program, with South Tangerang and Tangerang experiencing demand growth of 84% and 41% quarterly in the last quarter. This was followed by the Bandung area, where Bandung and Cimahi saw a demand growth of 38% and 36%, underscoring the increasing appeal of residences in the regions.

-

Locations such as Bogor, Tangerang, and Bekasi have become hotspots for demand, with the construction of the Serpong-Bogor toll road via Parung further enhancing Bogor Regency's appeal as a new residential destination. This demonstrates how infrastructure can influence demand patterns, with increased accessibility strengthening the property market position in the region.

Even though

new houses priced above IDR 5 billion

are not covered by the VAT exemption program, there has been significant quarterly demand

growth up to 2x

in the last quarter of 2023 in Bogor and Tangerang Raya, indicating that luxury houses in strategic locations remain in demand, regardless of fiscal incentives.

Surge in demand triggered by significant infrastructure development, a similar phenomenon has previously occurred in the Tangerang Raya area where demand in the fourth quarter of 2023 doubled compared to the same quarter in 2022.

The well-established infrastructure in the Tangerang Raya area continues to drive demand for both new and second-hand houses. Moreover, the Ministry of Public Works and Housing (PUPR) plans to accelerate the construction of the Serpong-Balaraja toll road, which currently in stage 1A, aiming to progress to stages 1B, 2, and 3 up to Balaraja by 2024.

+72%

+72% Reflecting on the surge in new houses demand in Bogor Regency-which reached 72% in the third quarter of 2023-

stimulated by significant infrastructure development,

such as Serpong-Bogor via Parung toll road development.

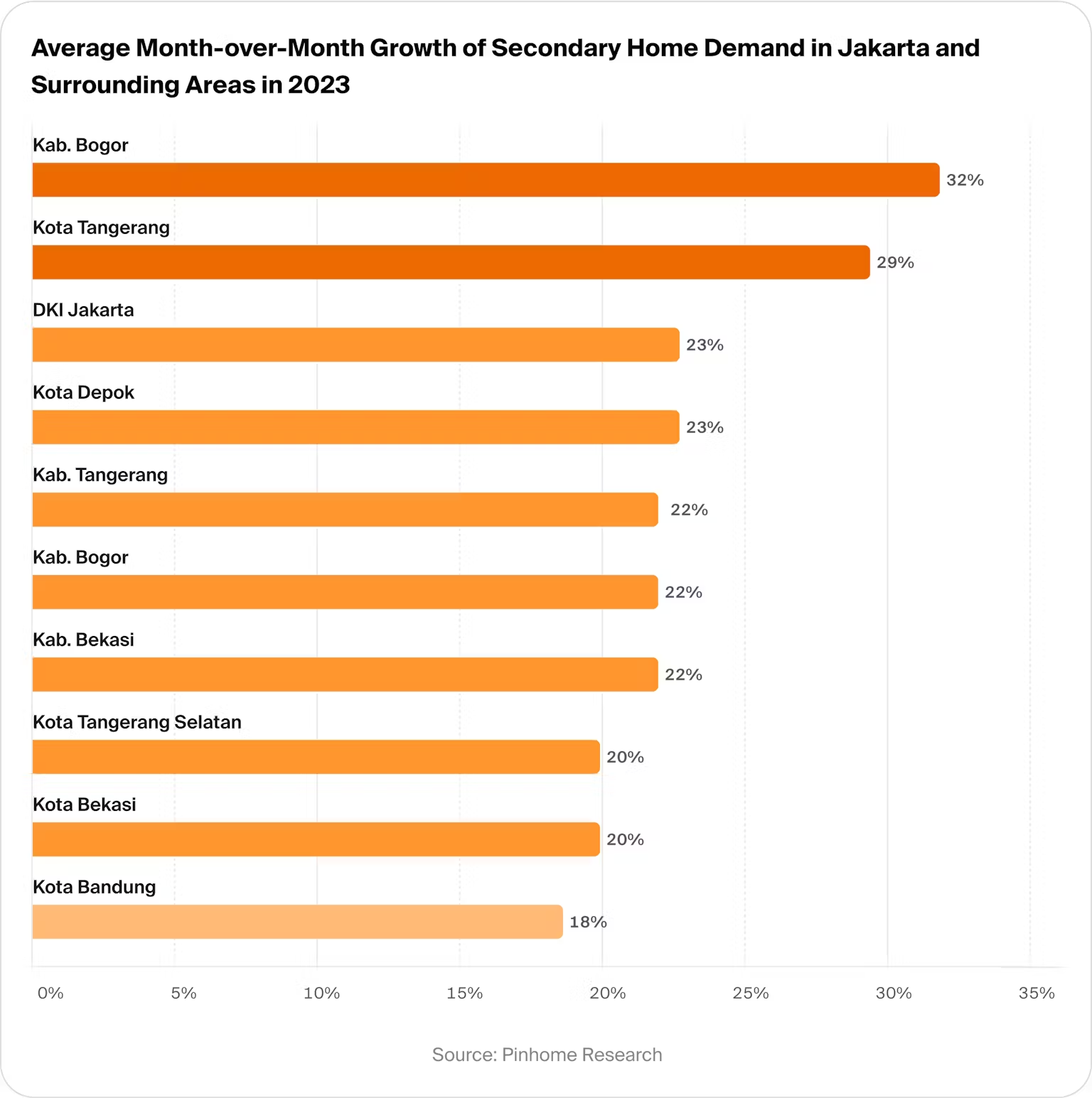

The demand for second-hand houses showed a consistent growth trend throughout 2023, except during long national holidays. DKI Jakarta and Bandung as well as surrounding cities such as Depok, Bekasi, and South Tangerang remain the top choices for second-hand home buyers, highlighting the sustained appeal of urban residences.

Outside of DKI Jakarta and its surrounding area, Bali also shows a consistent growth throughout 2023, with an average monthly growth rate reaching 25%.

Home Financing Adaptations Amid 2023 Interest Rate Fluctuations

Amid dynamic economic conditions and market responses to global monetary policies – The Federal Reserve’s interest rate hikes, Indonesia adjusted the interest rates for Home Ownership Loans (KPR) throughout 2023. These conditions spurred a strategic shift in KPR and KPR Take Over demand throughout the year, with buyers increasingly opting for shorter installment tenures to reduce long-term interest burdens.

Shift towards Shorter Loan Repayment Tenure

Gradually, from the first quarter to the last quarter, 25% of the total demand shifted from 16-20% year installment tenures to 11-15 year tenures.

Shift towards Longer Fixed Interest Rate Tenure

As of March 2023, following the interest rate hike by The Fed in February 2023, there was a surge in demand for 5-8 year fixed rate tenure in the KPR Take Over program by 28%, which is a shift in demand towards shorter fixed-rate tenures.

Significant Increase in KPR Take Over Demand

in July 2023, the number of KPR Take Over demand requests doubled, signaling the market’s adaptation to changing economic conditions. This was accompanied by increased interest in 10-year fixed-rate tenures in KPR Take Over programs, especially after the interest rate hike by The Fed at the end of July.

In 2023, the fixed interest rates for KPR transactions for the new and second-hand houses market in Pinhome platform ranged from 4.00% to 5.75%, while the fixed interest rates for KPR Take Over were slightly higher, between 4.50% to 6.25% for a three-year tenure.

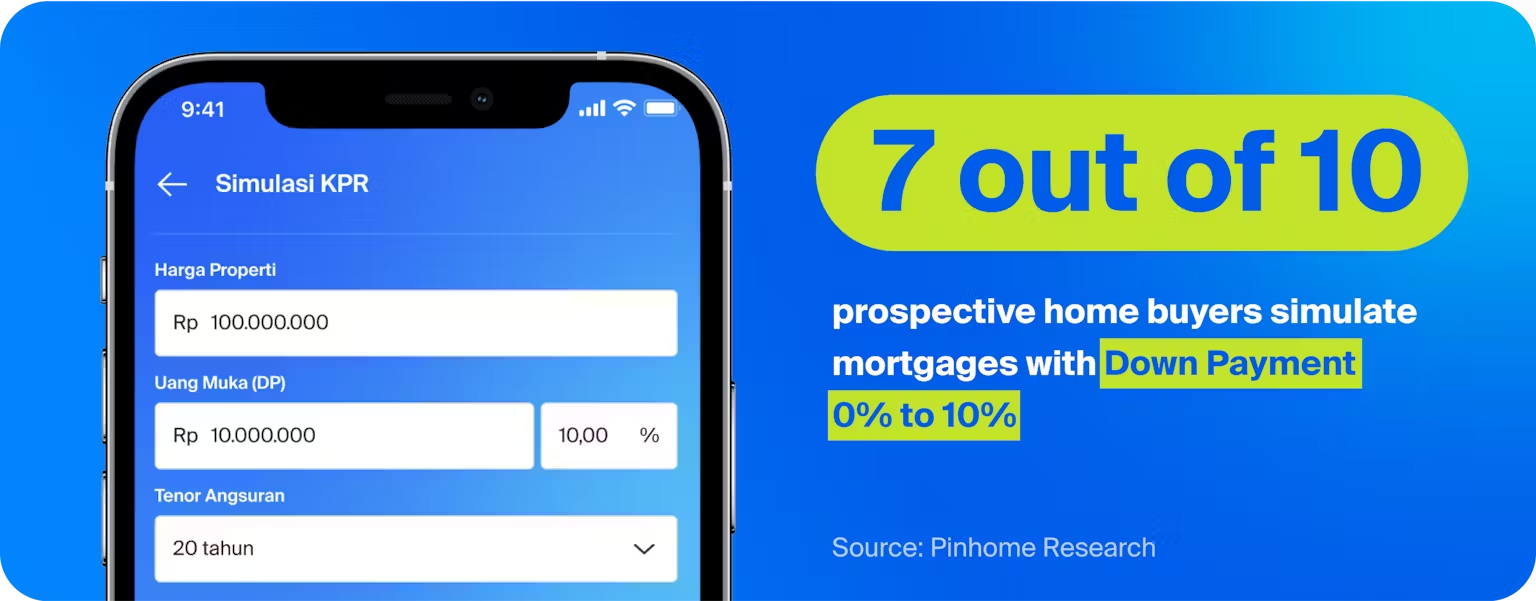

7 out of 10 prospective home buyers on Pinhome’s platform simulate KPR with down payment options ranging from 0% to 10%. This highlights the enthusiastic response from first-time homebuyers, including those from low-income communities (MBR) and younger generations or millennials, as a response to

-

Minister of Public Works and Public Housing (PUPR) decision No.995/KPTS/M/202 regarding interest rates applied below 5.00%, a 1% down payment, and a down payment assistance of IDR 4 million,

-

Bank Indonesia Governor’s Council Meeting (RDG) held on October 19-20, 2022, concerning the extension of the 0% down payment policy for KPR and Personal Loans (KTA) banking products from January 1 to December 31, 2023.

This further conveys the importance of access to tailored financing options for first-time homebuyers.

Urbanization and Post-Pandemic Rental Demand

The positive momentum post-pandemic, marked by the normalization of mobility and companies reinstating Work From Office (WFO), has driven an increase in urbanization and strengthened optimism towards the rental house market. Throughout 2023, the inventory of rental homes grew positively by 104% (Year-over-Year). This was marked by positive monthly growth despite a temporary decrease during Eid al-Fitr and November. Particularly in the provinces of Banten and West Java, there was a significant surge, with inventory growing up to twofold.

Popular Demand for Rental Homes in Metropolitan Areas and Surrounding Cities

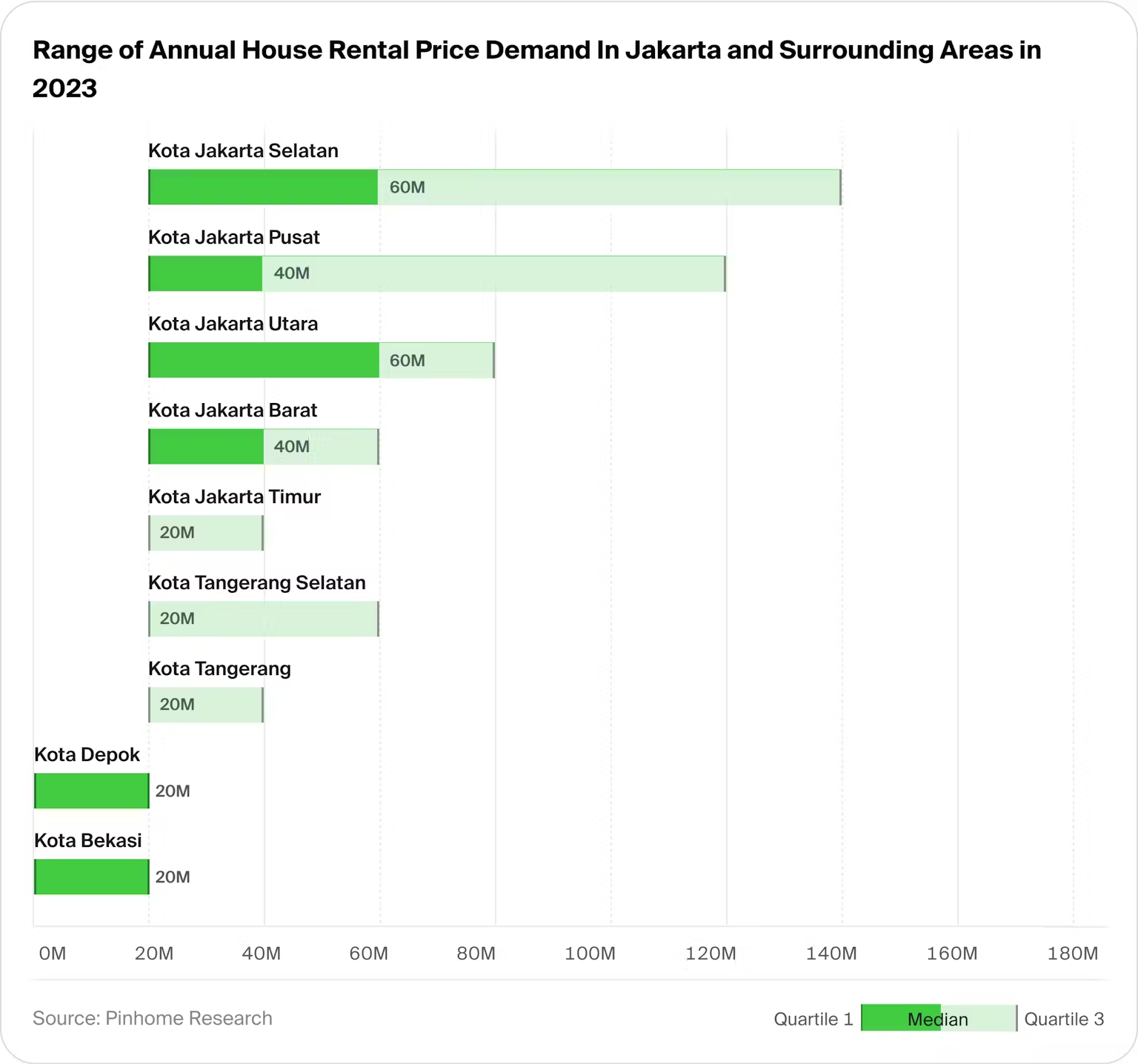

With the rise in urbanization, metropolitan cities such as DKI Jakarta and Bandung, as well as satellite cities like South Tangerang, Depok, and Bekasi, remain the top locations for renting houses. In these areas, the demand for rental houses shows a wide range of prices, reflecting the need for modest to upper-middle rental houses.

-

The interest of rental prices in DKI Jakarta vary. Generally, the rental prices for houses in South Jakarta and North Jakarta are at IDR 60 million per year, while Central Jakarta and West Jakarta are at IDR 40 million per year, and East Jakarta is at IDR 20 million per year.

-

Rental prices in Jakarta's satellite cities range up to IDR 20 million per year, offering affordable housing options for those seeking alternatives close to the capital city.

Citting the

Property Perspective from Gen Z 2023survey released by Jakpat, it was revealed that 36% of respondents prefer renting over buying due to not being financially ready. Other reasons include more affordable rental prices (22%) and the ability to choose strategic locations (18%). Furthermore, one out of three respondents chose to pay rent on a monthly basis.

Market Outlook 2024: Optimism in the Property Sector

Positive Boost from Infrastructure Development in Tourism Sector Recovery

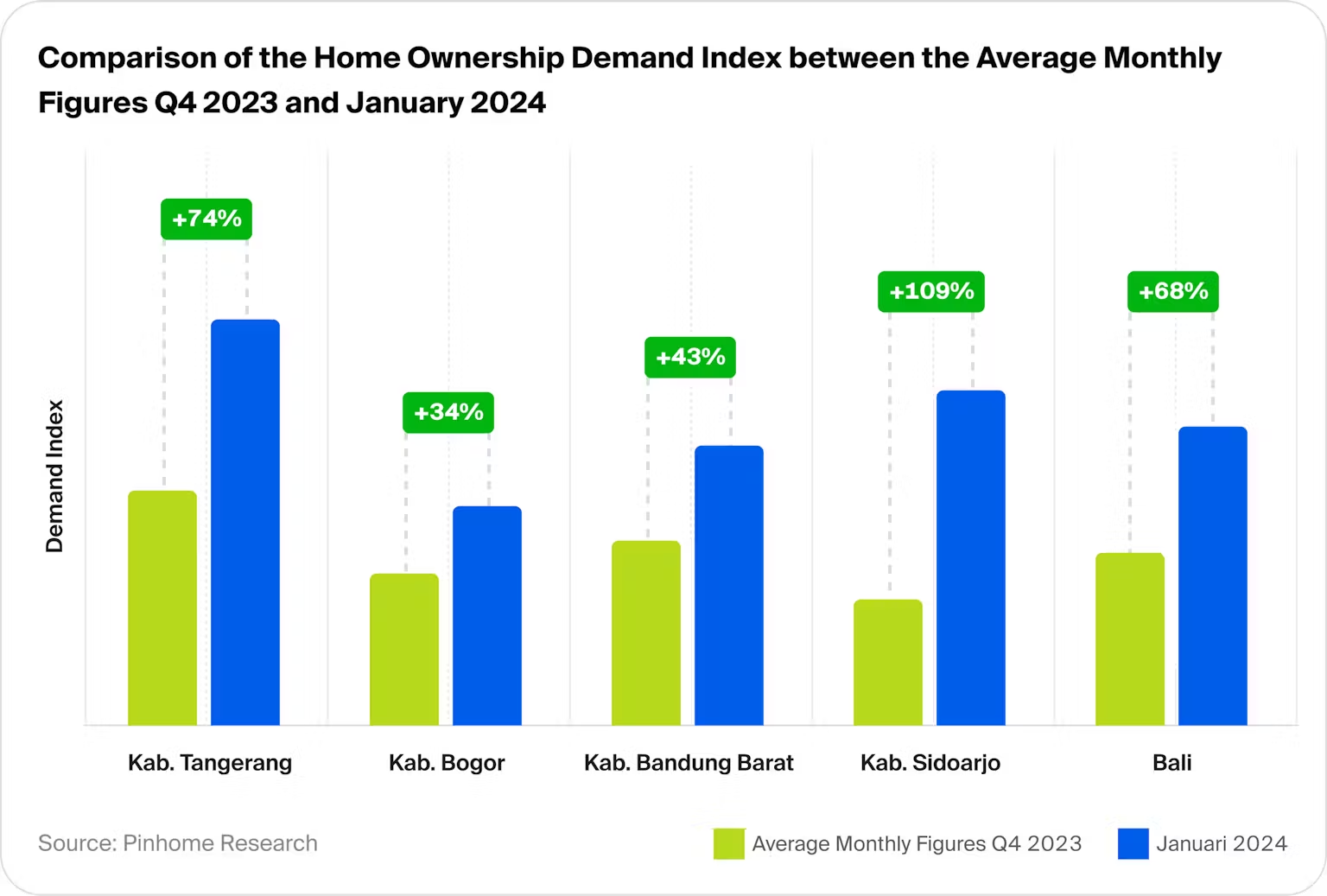

Entering the year 2024, Pinhome projects a positive trend in demand for new affordable houses priced below IDR 500 million, particularly in areas around DKI Jakarta expected to benefit from significant infrastructure development and in Bali, driven by the recovery of the tourism sector.

-

Tangerang Regency, bordering South Tangerang, where adequate infrastructure is available for prospective new house buyers. Furthermore, the accelerated development of the Serpong-Balaraja toll road up to section 3 is expected to expand the demand surge opportunities to Lebak Regency.

-

In Bogor Regency, Pinhome projects continuous demand growth in 2024, following the progress of the Serpong-Bogor toll road construction via Parung nearing completion.

-

In the Greater Bandung area, the Jakarta-Bandung high-speed train not only plays a role in reducing travel time between the two metropolitan cities but also promotes the development of facilities and infrastructure around the departure stations, especially in West Bandung Regency

-

In East Java, particularly in Sidoarjo Regency bordering Surabaya City, a growth in new house demand is projected for 2024. Its proximity to Surabaya city center offers unique advantages for Sidoarjo, yet still providing more affordable house prices. Additionally, the Ministry of Transportation plans to continue evaluating the Jakarta-Surabaya semi-fast train project in 2024, expected to enhance the attractiveness of Surabaya and its surrounding areas as residential destinations.

-

The recovery of the tourism sector significantly boosts the demand for new homes in Bali. The resurgence of this industry not only entices domestic investors but also captures the attention of foreign investors, who now see Bali as a highly promising investment location. The implementation of the golden visa policy by the Indonesian government, designed specifically to attract foreign investors, has played a crucial role in facilitating international investors to acquire property in Bali. This policy further strengthens Bali’s position as a favorite destination for property investment in 2024.

In analyzing search trend data with area as keywords, there was a significant growth in demand for second-hand houses in the cities of Balikpapan, Batam, and Medan, with an increase of more than 100% from the last quarter of 2023 to January 2024. This indicates local economic growth happens not only on the islands of Java and Bali.

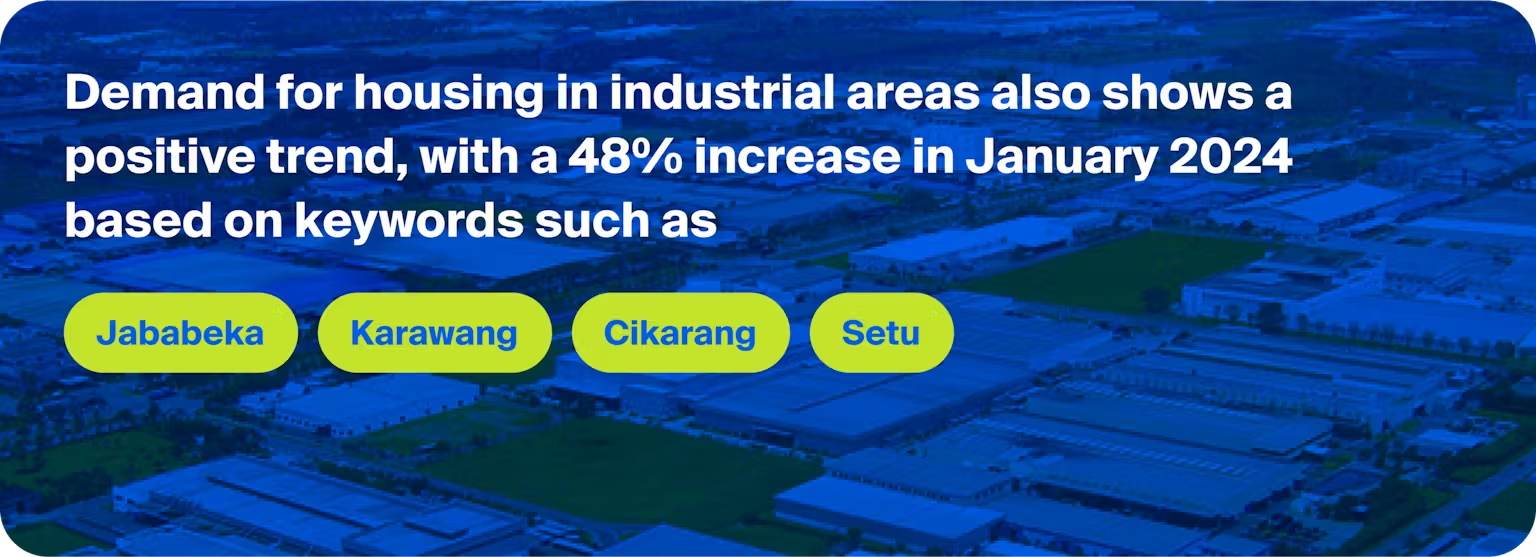

Positive Trend in Housing Demand in Industrial Areas

The Association of Industrial Estate reports a 46% increase in industrial land sales from January to September 2023 compared to the same period last year. Furthermore, driven by the realization of stronger investments in the industrial sector throughout 2023, the demand for housing in industrial areas is predicted to continue its positive trend in 2024.

Efforts to Secure Alternative Housing

Besides the increased demand prospects in several regions, a positive trend is also seen in consumer preferences in the effort for obtaining housing alternatives. Trend analysis of search data from the last quarter of 2023 to January 2024 shows that consumers are increasingly open to alternatives like house over-credit methods, due to that offers prospective homebuyers more affordable prices. Meanwhile, renting remains an option for consumers seeking flexibility in 2024.

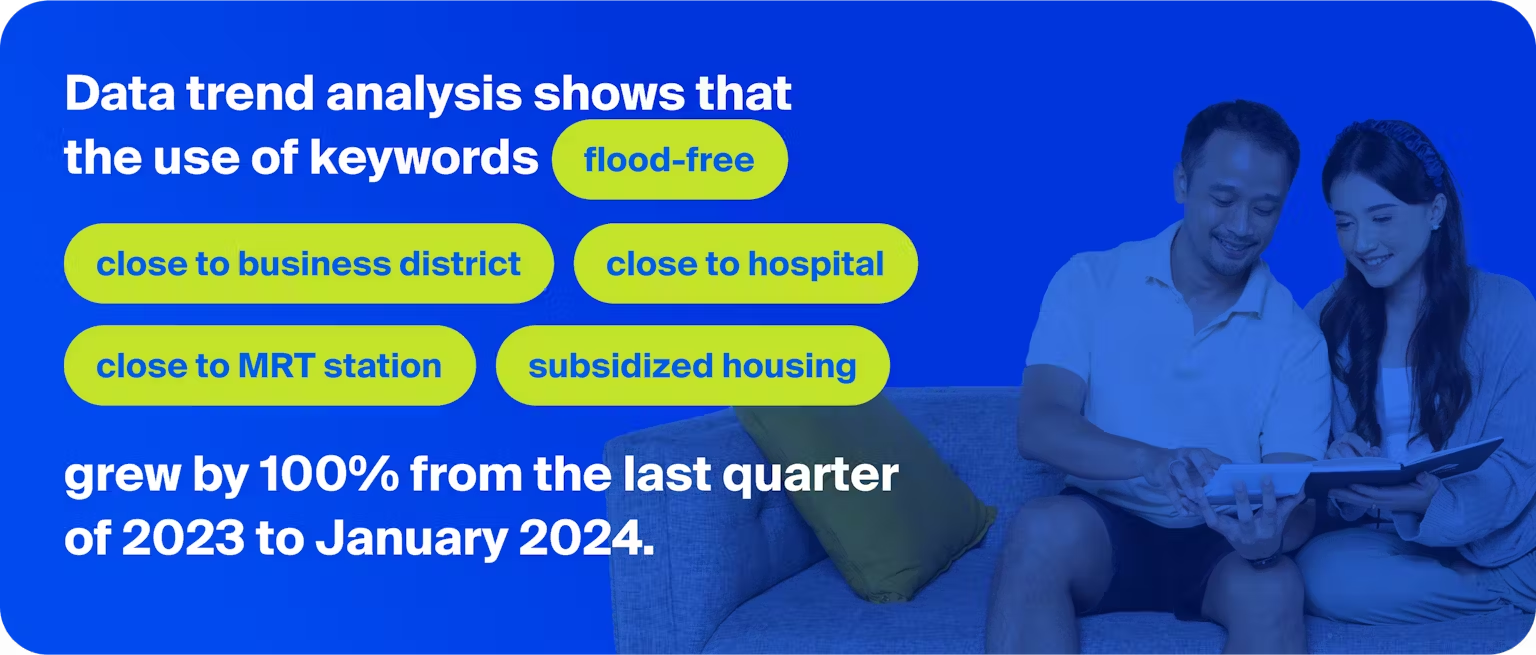

Preferences for Flood-Free Risk, Accessibility, and Affordability Remain Key Factors for Prospective Home Buyers in 2024

Projection of Decreased in Demand during Ramadan and Post-Eid al-Fitr Recovery

In Ramadan 2024, Pinhome projects that the demand for residential homes will remain stable for a few weeks before Ramadan and there will be a downward trend during the Ramadan period. Reflecting on Ramadan 2023, demand was able to stay stable for 3 weeks before entering Ramadan (hereafter referred to as pre-Ramadan). However, the average weekly demand weakened by up to -34% during Ramadan and began to recover at Eid al-Fitr. Demand not only recovered but also exceeded pre-Ramadan demand two months after Eid al-Fitr.

About Pinhome Indonesia Residential Market Report & Outlook

Pinhome Indonesia Residential Market Report & Outlook is an annual publication offering an in-depth analysis of the residential market dynamics. It provides insights on housing inventory (supply), buying and rental demand trends, as well as dynamics in financing demand based on the latest data from the previous year and projections for the residential industry for the upcoming year. Designed to fulfill the needs of industry players, policymakers, and the general public, this report aims to provide a comprehensive guide in understanding the residential industry market trends.

Methodology

The report’s underlying data comes from Pinhome’s extensive database, encompassing over 1 million housing inventories and partnerships with more than 20 banks and financial institutions. Augmented with reliable external data, it is synthesized and analyzed using various statistical methods to produce insights in national and regional scope. Insights into housing inventory provide a framework for tracking supply evolution in the market. The section on buying and rental demand offers a perspective on trends from the buyers’ and renters’ side, complete with potentially influential background momentum. Meanwhile, insights into the demand for home purchase financing reveal growth and shifts in consumer preferences towards financing options, such as Home Ownership Credit (KPR) and KPR Take Over. Projections for demand growth trends for the coming year are built on a comparison of demand growth data in January 2024 with the monthly average in the last quarter of 2023.